Discover Benefits, News, & More

Helping REALTORS® Take Their Business To The Next Level

For over a hundred years we have been helping REALTORS® transform their businesses from where they are to where they want to be. The Greater San Diego Association of REALTORS® is your trusted partner and truly dedicated to helping you succeed.

News & Press Releases

2026-04-30

SDAR URGES CONSUMERS AND REAL ESTATE PROFESSIONALS TO BE VIGILANT AS SCAMMERS IMPERSONATE LICENSED AGENTS

San Diego, Calif. — The San Diego Association of REALTORS® (SDAR) is alerting consumers and real estate professionals across San Diego County to a growing scam in which bad actors impersonate licensed California real estate agents to conduct fraudulent transactions.

According to the California Department of Real Estate (DRE), scammers are using the names, license numbers, photos, and professional identities of legitimate real estate agents and brokers to create fake online profiles, including social media accounts and property listings on platforms like Craigslist and TikTok. These impersonators then attempt to engage in illegal real estate activities such as fraudulent home sales, rental scams, and property management schemes.

How the Scam Works

Fraudsters are leveraging publicly available information to convincingly pose as licensed professionals. With minimal effort, they can create fake websites, email addresses, and online listings that appear legitimate. In many cases, scammers also fabricate business addresses or use unrelated physical locations to further deceive consumers.

Warning Signs to Watch For

SDAR encourages the public to be cautious of the following red flags:

Requests for upfront fees before services are rendered

Demands for cash payments or wire transfers

Communication from agents who cannot be verified through official channels

Listings or offers that seem unusually favorable or urgent

How to Verify a Real Estate Professional

Consumers are strongly advised to take the following steps before engaging in any real estate transaction:

Look up the agent’s license on the official DRE website.

Independently locate the agent’s office phone number through a trusted directory.

Call the brokerage directly to confirm the agent’s affiliation.

Verify that photos, contact information, and credentials match across official platforms.

What to Do If You Suspect Fraud

If you believe you have encountered or been a victim of this scam, report it immediately to the appropriate authorities, including:

The Internet Crime Complaint Center (IC3)

The California Department of Real Estate

The California Attorney General’s Office

Local law enforcement agencies

The Federal Trade Commission (FTC)

The Federal Bureau of Investigation (FBI)

The Consumer Financial Protection Bureau

Guidance for Real Estate Professionals

SDAR also advises its members to take proactive measures to protect their identities:

Regularly search your name and license number online

Monitor financial accounts and credit reports

Issue cease-and-desist notices if impersonation is detected

Protecting Our Community

“Protecting consumers and maintaining trust in the real estate profession is a top priority,” said SDAR President, Karen Van Ness. “We encourage everyone—buyers, sellers, renters, and agents—to remain vigilant and verify before they transact.”

Media Contact:

San Diego Association of REALTORS® (SDAR)

Kelly Christensen, [email protected]

2026-04-30

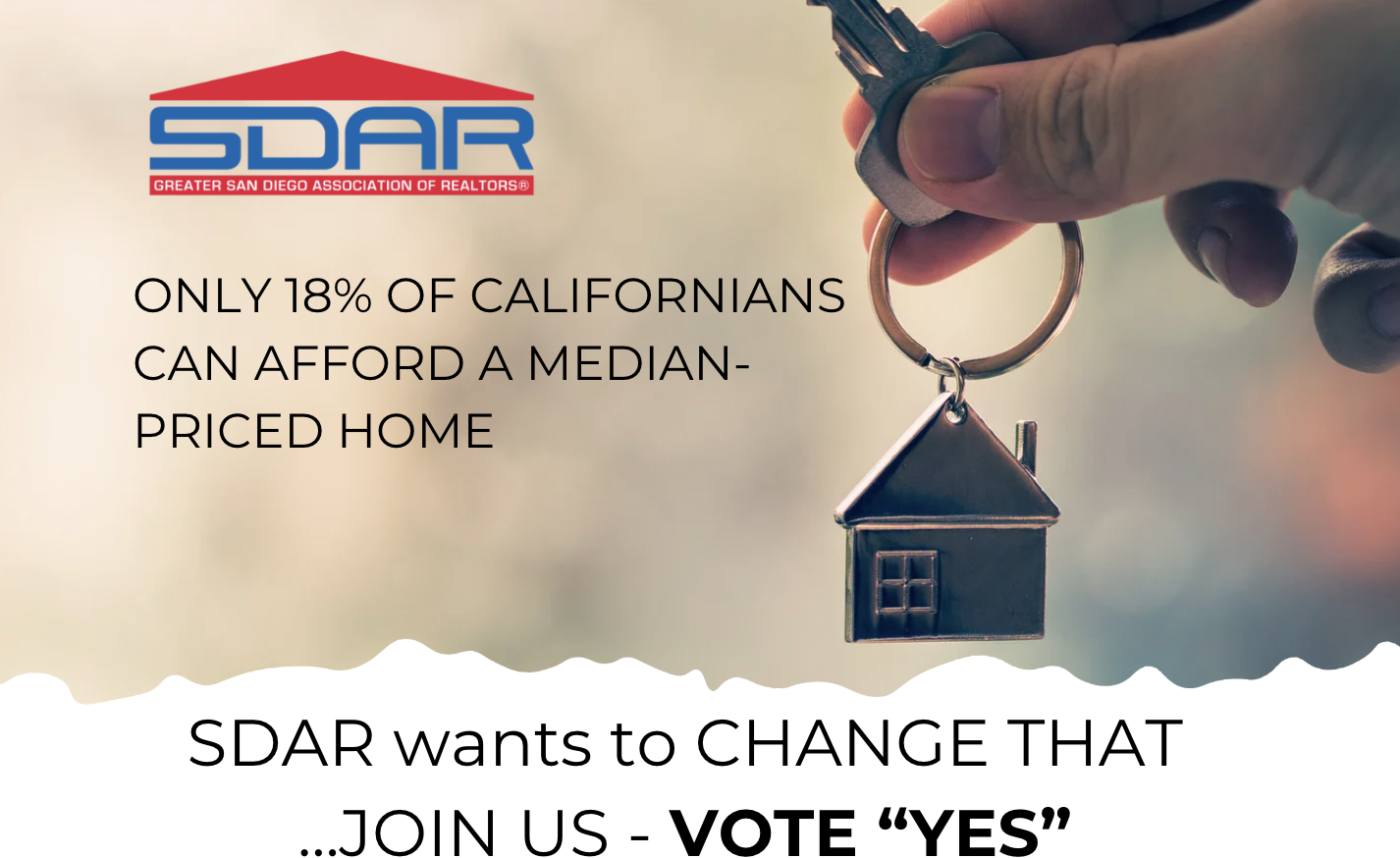

Expanding the Dream of Homeownership in California

Leaders from the San Diego Association of REALTORS® were recently in Sacramento advocating on key housing issues—including strong support for the California Dream For All Program.

This program is a game-changer for first-time buyers, helping bridge one of the biggest barriers to homeownership: the down payment.

It matters because it:

Provides up to 20% of a home’s purchase price (up to $150,000) for down payment or closing costs

Focuses on first-generation and first-time homebuyers

Helps close the wealth gap and expand economic mobility

Is structured as a revolving fund, supporting future buyers as homes are sold or refinanced

The reality:

Only 18% of Californians can afford a median-priced home

Homeownership rates continue to decline—especially among underserved communities

Demand for this program has been overwhelming, proving the need is real

SDAR's Position: Continue funding the California Dream For All Program

Homeownership shouldn’t be out of reach for hardworking Californians. Programs like this create real pathways to stability, equity, and generational wealth.

SDAR remains committed to advocating for solutions that make homeownership more attainable for all.

For more on this program, watch this Video!

2026-04-29

SDAR Supports California Middle-Class Homeownership and Family Home Construction Act of 2026

Sacramento, CA — During the recent C.A.R. Legislative Days in Sacramento, leaders from the San Diego Association of REALTORS® joined housing advocates and policymakers to support the California Middle-Class Homeownership and Family Home Construction Act of 2026, a statewide ballot initiative aimed at expanding access to homeownership for working Californians.

The proposed measure addresses one of the most significant barriers to homeownership: the down payment. By authorizing up to $25 billion in revenue bonds—not funded by taxpayer dollars—the initiative would provide qualified buyers with access to a state-backed second mortgage covering up to 17% of a home’s purchase price, helping bridge the gap for middle-income families who can afford monthly payments but struggle to save for upfront costs.

“California’s housing crisis demands real solutions,” said Karen Van Ness, President of SDAR. “This initiative is designed to increase homeownership opportunities, streamline development, and prioritize housing for working families—all without placing additional burden on taxpayers.”

Why This Matters:

Only a small percentage of California families can afford a median-priced home

Down payments exceeding $170,000 remain a major barrier

The initiative creates a pathway to 20% equity at purchase, eliminating the need for costly private mortgage insurance

Funding is repaid through homeowner mortgage payments—not the state’s General Fund

The measure is expected to appear on the November 2026 ballot, giving California voters the opportunity to directly shape the future of housing affordability in the state. SDAR emphasizes that expanding access to homeownership is critical to strengthening communities, closing the wealth gap, and ensuring long-term economic stability for families across California.

Van Ness urges the public to "contact your local and state representatives and express support for policies that expand housing access and remove barriers to homeownership. Your voice and your vote play a critical role in shaping the future of housing in California."

For more information or to get involved in advocacy efforts, please contact the San Diego Association of REALTORS® at 858-715-8000 and ask for Government Affairs Deputy Director, David Martin.

Classes & Events

Classes

New Member Orientation - Jul. 10

Are you a newly licensed real estate agent? If you are fresh out of real estate school, you are probably thrilled that you passed the test and found a great broker but have no idea what to do next! Join us for our live new member orientation at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

Classes

CRS One Day Course: Zero to 60 Home Sales a Year (and Beyond)

Do you dream of selling 60 homes or more per year, but aren't sure where to begin? Whether you are looking to jumpstart your business or just starting out, the RRC One Day Course, Zero to 60 Home Sales a Year (and Beyond) will help you accelerate your home sales and create a continuous flow of business. Learn new marketing methods that will help you position yourself as the REALTOR® of choice in your area. Join Matthew Rathbun, CRS is a Virginia licensed broker and executive vice president of Coldwell Banker Elite. He has served as an association director of education and president of Four Pillars Education. As a residential REALTOR®, Rathbun is a reoccurring high producer. Rathbun teaches a variety of national designation courses, broker-manager courses, and risk reduction programs. He also teaches regularly for Coldwell Banker Corporate and provides consulting services for one of the most innovative learning tools in the industry.

Classes

Essentials for New Agents - Series 1 of 6

This course covers everything from mastering the MLS and understanding the benefits of SDAR, to navigating contracts and managing conflicts, this class equips you with the foundational knowledge to thrive in the real estate world.

Classes

Sep 25 - Unlocking ADU Potential (Part 2)

Attend an engaging and comprehensive class on Accessory Dwelling Units (ADUs), presented by Lisa De Jesus of ADU Gurus. This special event will be held in two informative sessions this June, designed to provide you with the essential knowledge and tools to navigate the exciting opportunities in ADU development. Whether you are interested in adding value to single-family parcels or exploring multi-family options, our expert presenters will guide you through the latest legislative updates, building requirements, and strategic considerations. Attending both sessions is crucial to gain a complete understanding and make the most of this growing trend in California real estate. Don't miss this opportunity to expand your expertise and stay ahead in the market!

Classes

Sep. 29 - Social Media Training with Jason Pantana

Jason Pantana is a coach, trainer, and speaker for Tom Ferry International the world's leading real estate coaching program. His energetic style engages his audiences to utilize the ever-changing marketing tools of today.

Classes

Nov. 7 Webinar - Reading Preliminary Title Reports

Among the dozens of records that inform or disclose to the buyer significant knowledge about the property, the title report is one of the most important. In this webinar, Kevin Burke, JD, shows you how to read the preliminary title report.

Classes

Nov. 9 Webinar - Residential Listing Agreement

Next to the Purchase Agreement, the C.A.R. Residential Listing Agreement (Exclusive Right to Sell) is the most commonly used contract by REALTORS®. Join MIke Shenkman, UCSD professor, to learn the terms of this agreement and overcome the three common objections (commitment, price and commission) sellers have to signing the agreement.

Classes

Nov. 14 Webinar - Property Tax Explained: Prop. 13

In 1978, California voters overwhelmingly approved Proposition 13 in response to the dramatic increase in property tax. This proposition has received nationwide attention being the most famous and influential of California's ballot measures. Learn the history and impact of Proposition 13 with UCSD instructor, Mike Shenkman.

Classes

Nov. 15 - San Diego 2024 Forecast

Steven Thomas from "Reports on Housing" will break down the housing market from 2023 and bring his key insights and data to forecast what's to come on the horizon in 2024. Steven and "Reports on Housing" have delivered local data and forecasting services across Southern California for years, and is looking forward to answering all your real estate questions, like: When will rates drop and improve affordability? When will more homes come on the market? Will there ever be more foreclosures? We hope you can make it to learn more about the San Diego County housing market and where it's headed in 2024!

Classes

Nov. 21 Webinar - NHS Pro: More Leads, Less Effort

This webinar addresses and shares a solution to the most critical residential real estate issue general real estate agents face: a shortage of resale listings and the need for salable inventory. Plan to leave with an idea (that you can use the same day) that may help you make a sale you would have missed.

Classes

Nov. 30 - Ai-Powered Digital Domination in RE

Ready to supercharge your real estate and mortgage game with Artificial Intelligence (Ai)? Join this Google master class and discover how Ai-driving SEO, Google listings, and geo-tagging can boost your visibility. Use Ai to create SEO-friendly service descriptions, FAQs, and review responses. Held live in the classroom at SDAR's Kearny Mesa headquarters. Note: The deadline to sign up for this class is two days prior.

Classes

New Member Orientation - Dec. 5

Are you a newly licensed real estate agent? If you are fresh out of real estate school, you are probably thrilled that you passed the test and found a great broker but have no idea what to do next! Join us for our live new member orientation at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

Classes

Dec. 7 Webinar: Disclosures - Statutory vs. Contractual

REALTORS® are faced with countless contracts throughout the course of their career. These trainings are designed to inform, prepare and hone your skills to help you better serve and protect yourself and your clients. Kevin M. Burke, JD, keeps you in the loop with fast, easy and comprehensive real estate contract trainings

Classes

Dec. 14 Webinar: Creating the Ultimate Listing Agreement

Now, it's time to create the Ultimate Listing Agreement to "wow" your clients. Join Kevin Burke, JD. to learn all the tips and tricks on how manage your risk and win clients.

Classes

Dec. 17 - Mastering the Fundamentals of the MLS

Elevate your real estate expertise with "Mastering the Fundamentals of MLS," a class meticulously designed to turn the Multiple Listing Service into your most powerful tool. In this course, you'll unravel the complexities of MLS, learning to leverage its full potential to serve your clients effectively and efficiently. We'll cover the essentials of navigating listings, optimizing search strategies, and mastering the art of presenting data that captures attention. This isn't just about understanding a system; it's about transforming information into opportunities and using MLS insights to anticipate market trends.

Classes

Dec. 17 - Dominando los Fundamentos de MLS (en Espanol)

Eleva tu experiencia en bienes raíces con “Dominando los Fundamentos de MLS”, una clase diseñada meticulosamente para convertir el Servicio de Listado Múltiple en tu herramienta más poderosa. En este curso, desentrañarás las complejidades de MLS, aprendiendo a aprovechar todo su potencial para servir a tus clientes de manera efectiva y eficiente. Cubriremos los aspectos esenciales para navegar entre los listados, optimizar estrategias de búsqueda y dominar el arte de presentar datos que capturan la atención. Esto no se trata solo de entender un sistema; se trata de transformar la información en oportunidades y usar las percepciones de MLS para anticipar las tendencias del mercado.

Classes

Feb. 15 - The AI Age of Real Estate

Dive into this transformative class crafted for REALTORS® who are ready to harness the revolutionary power of artificial intelligence (AI) in their business strategy. This course will guide you through the latest AI tools and techniques that are reshaping the property market, ensuring your listings stand out in a competitive digital landscape. Learn how to automate your outreach, personalize client interactions, and analyze market data with precision -- all skills that will set you apart in the modern real estate industry. As you master these innovative solutions, you'll not only save time but also create more meaningful connections with buyers and sellers. Join us and be at the forefront of the AI revolution, where the future of real estate is not just predicted? It's already here.

Classes

Feb. 16 - REALTOR® Roundtable

Join the conversation at "REALTOR® Roundtable," where California's real estate professionals converge to sharpen their skills for the year ahead. This engaging class is a hub for collaboration, offering a deep dive into the state's latest real estate trends, legislation, and success strategies. Here, you'll exchange insights with peers, debate hot topics, and discover new approaches to common challenges in the ever-evolving property landscape. Each session is designed to empower you with practical knowledge and networking opportunities, ensuring you leave with a wealth of resources to elevate your practice. Whether you're looking to refine your expertise or expand your professional circle, this is your gateway to becoming a more informed and connected REALTOR® in 2024.

Classes

Feb. 23 Webinar - Get Paid What You're Worth!

Join us for a dynamic and captivating live webinar hosted by Jeff Mays of the Tom Ferry organization! Discover the secrets to turning potential leads into loyal, long-term clients who trust your expertise and rely on your services. Gain access to exclusive tools and strategies that will help you provide your buyers with a consultation experience that is second to none.

Classes

Mar. 6 - My Favorite Ai Tools for Real Estate

As we embrace technological advancements, it's crucial to stay ahead of the curve. Marketing and technology consultant CJ Brogan presents an informative tech talk: "My Favorite AI Tools for Real Estate!" Learn about cutting-edge Ai tools transforming real estate marketing, lead generation, and customer engagement. CJ cuts through all of the Ai noise and chatter out there to cast a spotlight on the easiest, most relevant, and cost-effective Ai tools and options for real estate out there.

Classes

Sep 5 - zipForm: Focusing on the RLA & RPA

Learn the critical details of the Residential Listing Agreement (RLA) and Residential Purchase Agreement (RPA) forms. Each form will be given dedicated attention with approximately one hour of focused instruction, ensuring you gain a comprehensive understanding of these essential documents. Learn the nuances that will help you navigate your transactions with confidence and clarity. Whether you're new to these forms or looking for a refresher, this class will enhance your proficiency in managing real estate contracts. Don't miss this opportunity to elevate your expertise and better serve your clients.

Classes

Sep 13 - zipForm: Focusing on Buyer Forms

In this class, our contract expert will guide you through the essential buyer forms used in real estate transactions including the Buyer Representation and Broker Compensation Agreement (BRBC).. Each form will receive dedicated attention, ensuring you gain a comprehensive understanding of how to effectively utilize these documents in your practice. Learn the nuances that will help you manage your listings with confidence and precision. Whether you're new to these forms or seeking a refresher, this class will enhance your proficiency in handling buyer agreements. Elevate your expertise and better serve your clients through this targeted instruction.

Classes

Sep 27 - California Prop 33: Rent Control

Gain a comprehensive understanding of California Proposition 33 in this informative session presented by the Southern California Rental Housing Association. Delve into the details of the rent control legislation to gain insights to navigate its impact on the rental market. The instructor will break down the complexities of the law, offering practical guidance on how it affects landlords, tenants, and the broader real estate landscape. Whether you're a property manager, landlord, or agent, this session will equip you with the knowledge to stay ahead in the evolving rental market.

Classes

Oct 29 - Building Strong Teams: Strategies for Success

This class explores key strategies for fostering a cohesive, productive team environment, where collaboration and communication excel. Instructor Zandra Ulloa shares expert insights on identifying strengths within your team, delegating tasks effectively, and maintaining motivation for sustained success. Whether you’re forming a new team or refining an existing one, this course offers valuable tools to enhance leadership and team dynamics. Gain actionable strategies to create a thriving team culture that drives exceptional results!

Classes

Dec 18 - Code of Ethics (Live in Kearny Mesa)

Based upon the NAR's Code of Ethics and Standards of Practice, learn about the standards of ethical conduct in the practice of real estate. This course also covers the California Business and Professions Code that guides ethical business practices within California. You will receive 3.00 of CE upon completion of the course and passage of the 15-question exam. Arrive 15 minutes early for registration and bring a government-issued ID for verification. Late registrants will not be allowed to enter the classroom. (DRE SPONSOR ID #0282)

Classes

Open House Procedures 30 January 2025: Time 11am -1pm

Discover how to make your open houses a client magnet with professional tips, preparation strategies, and standout presentation skills.

Classes

Week 6: Exceptional Service & Hospitality

Turning Clients into Raving Fans Elevate your client experience with service strategies inspired by the world’s most prestigious luxury markets. This session will teach you how to create unforgettable moments that exceed expectations and build lasting loyalty. Discover techniques to personalize your interactions, anticipate client needs, and deliver service that goes beyond the ordinary. Learn how to foster trust and create advocates who will enthusiastically promote your business. Transform your approach to client care and set a new standard of excellence that ensures every client becomes a raving fan.Week 7: Sweat Equity Explore creative strategies for maximizing property potential and creating win-win outcomes that benefit buyers and sellers alike.

Classes

Week 5: Negotiation Skills vs. A.I.

Showcasing Your Irreplaceable Value In an era where automation and artificial intelligence are rapidly reshaping industries, your ability to negotiate effectively can set you apart. This engaging session will equip you with advanced negotiation techniques to outshine the rise of automation and demonstrate your value as a skilled advocate. Learn how to build trust, navigate complex transactions, and address your clients' unique needs with human-centric strategies that A.I. cannot replicate. Discover practical tools to enhance your influence and secure better outcomes for your clients. Stay ahead of the curve by mastering the art of negotiation that keeps you indispensable in the ever-evolving marketplace.

Events

Hard Hat Tour - Snapdragon Stadium & SDSU Development

Join us for an exclusive Hard Hat Tour of the Snapdragon Stadium and SDSU/Avalon Mission Valley development, one of the most significant mixed-use projects in the region. Explore first-hand the evolving landscape of this dynamic development — including residential, retail, and strategic growth elements that are transforming Mission Valley.

March 24, 2026 | 3:00 – 4:00 PM

Networking to Follow | 4:00 – 6:30 PM

Tour Details:

• Date: Tuesday, March 24, 2026

• Time: 3:00 – 4:00 PM

• Location: Sycuan Pier inside Snapdragon Stadium

Networking Reception:

Immediately following the tour, enjoy an extended networking reception from 4:00 – 6:30 PM, featuring food and refreshments at a nearby venue (TBD). This is a great opportunity to connect with fellow commercial real estate professionals, developers, and industry partners.

Why Attend:

• Insider access to a major regional development

• Unique perspective on project design, planning, and market impact

• Networking with industry leaders, brokers, and investors

• Expand your commercial real estate insight and connections

Space is limited — don’t miss out on this valuable industry event!

Classes

Benefits Only

Join us for our Benefits Only at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

Classes

New Ethics Only

Based upon the National Association of REALTOR ®'s Code of Ethics and Standards of Practice, learn about the standards of ethical conduct in the practice of real estate. This course also covers the California Business and Professions Code that guides ethical business practices within California.<br /><br>Engage with scenarios that challenge and refine your ethical compass in a landscape where every decision impacts clients, community, and career. This course is more than a requirement; it's a commitment to upholding the highest standards of practice, ensuring that trust and respect are the foundation of your success.<br /><br />You will receive 3.00 of CE upon completion of the course and passage of the 15-question exam.<br /><br />Arrive 15 minutes early for registration and bring a government-issued ID for verification. Late registrants will not be allowed to enter the classroom.<br />

Classes

New Member JumpStart

Join us for our New Member JumpStart at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Events

Hybrid | Certified International Property Specialist (CIPS)

San Diego continues to be a top destination for global buyers and sellers. Don't miss the opportunity to expand your business internationally. Elevate your status in the global real estate market by earning your CIPS (Certified International Property Specialist) designation.

Join us for our 2025 in-person and virtual five-day program, offered on May 6, 7, 13, 14, and 20. The CIPS designation requires the completion of five full-day courses, each focusing on critical aspects of international real estate transactions. As a CIPS designee, you'll gain access to a powerful network of over 4,000 professionals who prioritize referrals and business partnerships.

Embrace the world of global real estate with the CIPS Designation.

All five classes will be available in person, via webinar, or both. If you prefer to complete the full designation online, you will receive a registration link after signing up here. Individual classes are also available.

NOTE: If you’re not an SDAR member please contact [email protected]

Classes

Unraveling The Mystery of 1031 Exchanges

This educational seminar will include a discussion of 1031 exchange issues from the Realtors® perspective such as qualified use and like-kind property requirements. (What really qualifies), reinvestment requirements (how much do you really need to reinvest), qualified trust accounts or qualified escrow accounts, 45 and 180 calendar day deadlines, identification rules and requirements, forward, reverse, improvement and foreign property 1031 exchanges.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Delivery Method Live Classroom

Classes

New Member JumpStart

Are you a newly licensed real estate agent? If you are fresh out of real estate school, you are probably thrilled that you passed the test and found a great broker but have no idea what to do next!

Join us for our New Member JumpStart at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

Proactive Property Management Tips

Proactive Property Management Tips is a practical course designed to provide real estate professionals with proactive property management tips and strategies that maximize efficiency and minimize risk. This training covers essential topics including the importance of thorough tenant screening, crafting legally sound lease agreements, and implementing effective rent collection strategies. You’ll also gain insight into navigating lease renewals, handling evictions professionally, and attracting quality tenants through smart marketing.

Events

Commercial Real Estate Pitch Session

The Commercial Real Estate Alliance of San Diego (CRASD) invites you to attend our upcoming Commercial Real Estate Pitch Session—a key event for professionals involved in the region’s active and evolving commercial market.

Don't miss the chance to expand your portfolio and explore business opportunities while networking with commercial real estate practitioners. Complimentary lunch is provided.

Please submit your pitch deal to David Martin for approval - [email protected]

Classes

New Member JumpStart

Are you a newly licensed real estate agent? If you are fresh out of real estate school, you are probably thrilled that you passed the test and found a great broker but have no idea what to do next!

Join us for our New Member JumpStart at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

Code of Ethics July

Based upon the National Association of REALTOR ®'s Code of Ethics and Standards of Practice, learn about the standards of ethical conduct in the practice of real estate. This course also covers the California Business and Professions Code that guides ethical business practices within California.

Engage with scenarios that challenge and refine your ethical compass in a landscape where every decision impacts clients, community, and career. This course is more than a requirement; it's a commitment to upholding the highest standards of practice, ensuring that trust and respect are the foundation of your success.

You will receive 3.00 of CE upon completion of the course and passage of the 15-question exam.

Arrive 15 minutes early for registration and bring a government-issued ID for verification. Late registrants will not be allowed to enter the classroom.

Events

Global Connections: International Cottages: Balboa Park

Hosted by SDAR’s International Real Estate Committee (IREC)In collaboration with the National Association of Hispanic Real Estate Professionals (NAHREP), the Asian Real Estate Association of America (AREAA), and the California Association of Real Estate Brokers (CAREB).

Join us for an engaging evening celebrating global connections and cultural diversity in the real estate industry.

The event will highlight 2025 initiatives aimed at promoting the City of San Diego internationally and will offer valuable networking opportunities with local organizations.

Discover how real estate professionals and associations are shaping San Diego’s future locally and internationally.

Food and Drinks Provided

* *NO REFUNDS for this event**

Please contact [email protected], for further questions or concerns.

Thank you

Classes

Unraveling The Mystery of 1031 Exchanges

This educational seminar will include a discussion of 1031 exchange issues from the Realtors® perspective such as qualified use and like-kind property requirements. (What really qualifies), reinvestment requirements (how much do you really need to reinvest), qualified trust accounts or qualified escrow accounts, 45 and 180 calendar day deadlines, identification rules and requirements, forward, reverse, improvement and foreign property 1031 exchanges.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

NAR's Senior Real Estate Specialist (SRES®) Designation

Online Only

The SRES® designation is the only real estate designation addressing the needs of today’s home buyers age 50-plus within your market. This unique designation is designed for the real estate agent who wants to focus on working with mature clients through major financial and lifestyle transitions. When you earn the SRES® designation you’ll learn how to:

Identify the power of generational demographics.

Develop and maintain marketing skills.

Counsel local seniors rather than selling the family home.

Use team-building skills with other SRES® professionals.

Understand the implications of tax laws, probate and estate planning.

Create a unique marketing opportunity that separates you from the competition.

You will also be listed online in the SRES® referral database which provides direct client contact and referrals from other SRES® designees.

To receive the SRES® designation:

Complete the two-day SRES® designation course.

Be in good standing with the National Association of REALTORS®.

Active membership in the SRES® Council. (New designees receive a one-year membership in the Seniors Real Estate Council® FREE. Annual dues are $99 each year thereafter.)

Events

CRASD Hard Hat Tour: HP Investors - Solana Beach Headquarters

Join the Commercial Real Estate Alliance of San Diego (CRASD) for an exclusive behind-the-scenes tour of HP Investors' latest project in the heart of Solana Beach!

In June 2022, HP Investors acquired the former Bank of America building, located at the prime corner of Hwy 101 and Dahlia Drive. This 8,296 SF commercial property was transformed into the company’s new headquarters. Be among the first to witness the evolution of this iconic space.

What to Expect:

Guided hard hat tour of the redevelopment project

Meet the HP Investors team

Learn about the project’s vision and strategic location

4:00 PM – 5:00 PM | Hard Hat Tour

5:00 PM – 7:00 PM | Networking at Solana Beach Kitchen

Limited Space Available - Reserve Your Spot Today!

(Tickets include Tour, Drinks and Appetizers)

Classes

Turbo-charge Your Business with Assumptions

Turbo-charge Your Business with Assumptions is an advanced training designed to give real estate professionals the tools and strategies to unlock the power of assumable loans in today’s market.

Led by Michael Lorino, Founder & CEO of AssumeList, and Nora Simpson, Head of Training, this class dives into the rules and regulations for VA and FHA assumptions, how to educate clients and agents, and proven methods to identify, market, and generate assumable listings. You’ll learn how to help buyers secure lower interest rates, overcome cash gaps, ensure servicers comply with the law, and navigate the four most common obstacles to closing assumptions—transforming this often-overlooked tool into a powerful competitive advantage.

Joining the instruction team is Jessica Mushovic, Chair of the IT and Business Technology Committee at the Greater San Diego Association of REALTORS® (SDAR). A dynamic leader driving innovation in the real estate industry, Jessica has played a pivotal role in advancing strategic partnerships, including SDAR’s collaboration with AssumeList, and brings her unique perspective on leveraging technology and business strategy to support REALTORS® in today’s evolving market.

Events

Member Appreciation Day!

Member Appreciation Day & the Annual Membership Meeting

Wednesday, Sept. 24 | 10 a.m. – 4 p.m.

Kearny Mesa Location — 4845 Ronson Ct. San Diego, Ca 92111

Join the SDAR Staff, Board Members and Volunteers for a fun block party-style day filled with delicious food, complimentary merch, and special events. Happening at our Kearny Mesa Offices, this event is FREE for all Members.

Member Appreciation Day Event Highlights

- Fire Hardening Update: Led by Jacqueline "Jackie" A. Oliver, Esq (10:00 am 11:30 am)

Election Winners Announced (11:45 AM – 1:00 PM)

Lunch & Annual Meeting

Responsible Use of Artificial Intelligence (AI) by Real Estate Licensees with Kathy Mehringer (1:30 PM – 3:00 PM)

As part of our Members First initiative, we’re excited to invite you to a special SDAR Member Appreciation Day — our way of saying thank you for your continued support and membership.

Classes

Code of Ethics

Based upon the National Association of REALTOR ®'s Code of Ethics and Standards of Practice, learn about the standards of ethical conduct in the practice of real estate. This course also covers the California Business and Professions Code that guides ethical business practices within California.

Engage with scenarios that challenge and refine your ethical compass in a landscape where every decision impacts clients, community, and career. This course is more than a requirement; it's a commitment to upholding the highest standards of practice, ensuring that trust and respect are the foundation of your success.

You will receive 3.00 of CE upon completion of the course and passage of the 15-question exam.

Arrive 15 minutes early for registration, have your SDAR Member # with you, and bring a government-issued ID for verification. Late registrants will not be allowed to enter the classroom.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Events

RUN. HIDE. FIGHT.

BE READY FOR THE UNEXPECTED

Learn proven, real-time strategies from FBI experts to protect yourself and others in critical moments.

Classes

10-key-relationships-to-6-figure-success-new

10 Key Relationships to 6-Figure Success is a transformative class that shows agents how to build a thriving, referral-based business by strategically nurturing just ten meaningful relationships. Led by veteran real estate leader and trainer Mike Marmion, this session reveals how to identify, engage, and sustain connections that consistently generate high-quality business and long-term growth. Learn how to create a simple, repeatable plan that turns your personal network into a powerful income engine for 2026 and beyond. Whether you’re a new or seasoned agent, you’ll walk away with practical tools and a focused strategy to achieve multiple 6-figure success through the power of purposeful relationships.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

Riches in the Niches: Winning Business in Today’s Market

Riches in the Niches: Winning Business in Today’s Market is a high-impact class designed to help real estate professionals stand out, specialize, and thrive — even in shifting market conditions. Led by industry veteran and master trainer Mike Marmion, this course explores 26+ proven niche strategies that can transform your business plan and expand your reach beyond your immediate sphere. Learn how to identify profitable niches, craft a simple vision and actionable plan, and generate consistent business from “people you don’t know.” Whether you’re building your brand or refining your focus, this session will equip you with the insight, direction, and confidence to create lasting success through strategic specialization.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

Open House FENG SHUI Staging

Open House FENG SHUI Staging introduces REALTORS® to the art and science of Feng Shui as a powerful tool to enhance property appeal and attract high-value offers. Taught by renowned Feng Shui Master Alex Zi—an expert with over 30 years of experience and more than 9,000 students worldwide—this course reveals how strategic design, color, energy flow, and timing can influence buyer perception and success at open houses. Using Feng Shui principles, learn how to stage every part of a home, balance the five elements, and resolve common layout challenges such as T-sections and stair placements. You’ll also discover how to apply Feng Shui to your marketing materials and client interactions to create harmony, confidence, and prosperity in your business.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

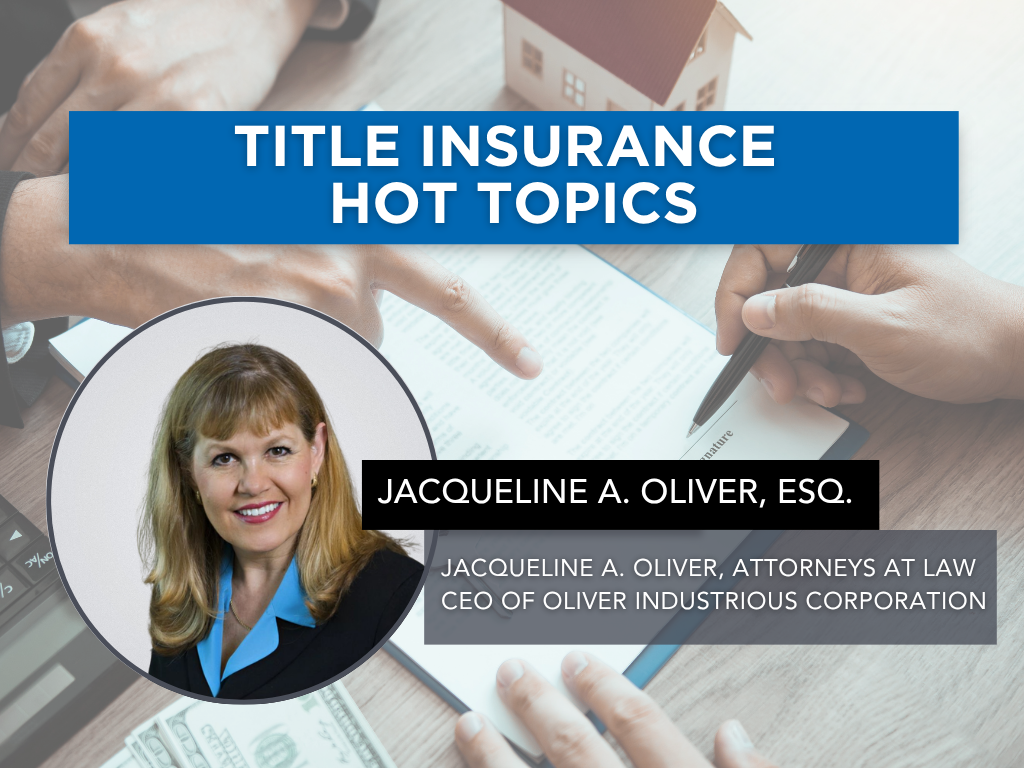

Confirmation Letters

Confirmation Letters is an essential risk management course for real estate professionals who want to protect themselves and their clients through proper documentation and communication. Taught by attorney, broker, and educator Jacqueline A. Oliver, Esq., this class explains how to create a written record of important conversations to prevent misunderstandings and potential legal disputes. Through real case studies and practical examples, agents will learn when and how to use confirmation letters, what to include, and how to apply them in scenarios involving disclosures, inspections, taxes, and employment issues. Gain the tools to avoid costly “he said/she said” situations and strengthen your professional credibility in every transaction.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

ZipForms: RPA's

Join us for an in-depth exploration of the "ZipForms: RPA's" class, where esteemed REALTOR® and contract expert Karen Van Ness will guide you through the critical details of the Residential Purchase Agreement (RPA) form. Learn the nuances that will help you navigate your transactions with confidence and clarity. Whether you're new to the RPA or looking for a refresher, this class will enhance your proficiency in managing real estate contracts. Don't miss this opportunity to elevate your expertise and better serve your clients.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

New Member JumpStart

Are you a newly licensed real estate agent? If you are fresh out of real estate school, you are probably thrilled that you passed the test and found a great broker but have no idea what to do next!

Join us for our New Member JumpStart at our Kearny Mesa office featuring training on what you need to know to get started, the benefits of your SDAR member products and services, and lunch provided by the top real estate affiliates.

Arrive 15 minutes early for registration, have your SDAR Member # with you, and bring a government-issued ID for verification.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

Code of Ethics

Based upon the National Association of REALTOR ®'s Code of Ethics and Standards of Practice, learn about the standards of ethical conduct in the practice of real estate. This course also covers the California Business and Professions Code that guides ethical business practices within California.

Engage with scenarios that challenge and refine your ethical compass in a landscape where every decision impacts clients, community, and career. This course is more than a requirement; it's a commitment to upholding the highest standards of practice, ensuring that trust and respect are the foundation of your success.

You will receive 3.00 of CE upon completion of the course and passage of the 15-question exam.

Arrive 15 minutes early for registration, have your SDAR Member # with you, and bring a government-issued ID for verification. Late registrants will not be allowed to enter the classroom.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

Unraveling The Mystery of 1031 Exchanges

This educational seminar will include a discussion of 1031 exchange issues from the Realtors® perspective such as qualified use and like-kind property requirements. (What really qualifies), reinvestment requirements (how much do you really need to reinvest), qualified trust accounts or qualified escrow accounts, 45 and 180 calendar day deadlines, identification rules and requirements, forward, reverse, improvement and foreign property 1031 exchanges.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 2 DAYS PRIOR*

Classes

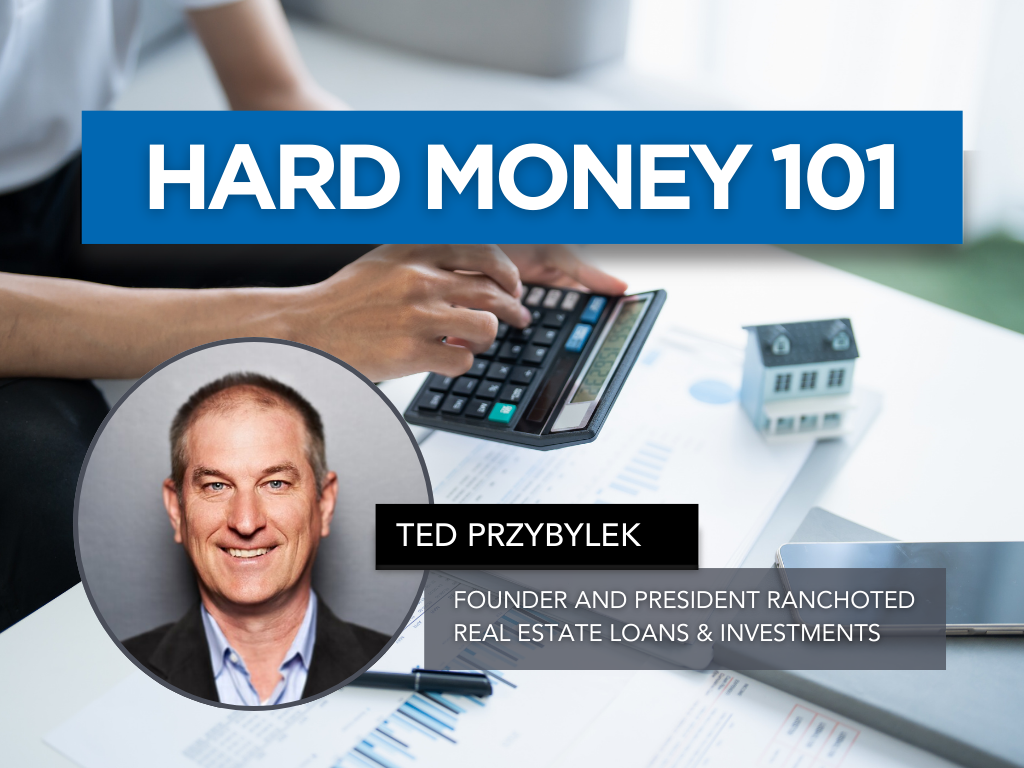

Hard Money 101

Hard Money 101 gives real estate professionals a clear, practical understanding of hard money lending—what it is, when to use it, and how it can help clients close transactions that traditional financing can’t support. Taught by lending veteran Ted Przybylek, i.e. Rancho Ted’, a 30+ year industry expert known for solving complex buyer and seller scenarios, this course breaks down asset-based lending, true bridge loans, investor-funded financing, and real-life case studies that illustrate when hard money is the right tool. Learn how to identify situations where speed, flexibility, or property conditions make hard money a smart solution, and gain the confidence to guide clients through alternative lending options that keep deals alive. This class is ideal for agents working with investors, flippers, distressed sellers, or buyers facing lending challenges.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Events

CIPS Designee Celebration

Join us for a special evening as we celebrate our Certified International Property Specialist (CIPS) Designees and the growing global real estate community in San Diego!

This event is open to:

Current CIPS Designees — come celebrate your achievements, reconnect with peers, and share your global success stories.

Aspiring Designees — discover how earning the CIPS designation can expand your network, elevate your business, and open doors to international opportunities.

REALTORS® and Industry Professionals — learn about the power of global real estate and how to position yourself in the international market.

Enjoy an inspiring program featuring highlights from our international initiatives, recognition of new designees, and conversations on global market trends shaping our industry.

Why Attend?

Celebrate San Diego’s global real estate leaders.

Network with international-minded REALTORS® and industry partners.

Learn how to earn your CIPS Designation and connect with clients around the world.

Enjoy light refreshments, lunch, drinks, and a lively atmosphere.

Don’t miss this opportunity to connect, celebrate, and grow your international reach!

Classes

Your 2026 Realtor Success Playbook

The Perfect 2026 Business Boost & Kickoff Plan is a high-energy, action-focused workshop designed to help REALTORS® launch the new year with clarity, momentum, and a simple plan that actually works. Led by renowned real estate coach and industry leader Mike Marmion, this course breaks down the essential activities that drive immediate business—open house strategies, sphere engagement, daily prospecting, relationship-building, and neighborhood conversations. Attendees will leave with a practical, easy-to-follow blueprint for boosting production, strengthening relationships, and accelerating their 2026 business from day one.

*THE DEADLINE TO SIGN UP FOR THIS CLASS IS 1 DAY PRIOR*

Classes

New Member Orientation

Start your real estate career with confidence at SDAR’s New Member Orientation. Designed for newly licensed REALTORS®, this essential session will walk you through everything you need to know to launch your business, understand your professional responsibilities, and make the most of your SDAR membership.

You’ll learn how to access and use your core member benefits, explore the tools and services included with your SDMLS subscription, and gain a foundational understanding of REALTOR® ethics, professional standards, and compliance requirements. The program also includes an overview of SDAR’s support teams, legal resources, market tools, industry advocacy, and opportunities for networking, education, and community involvement.

Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 2 days before the session.

Classes

Code of Ethics

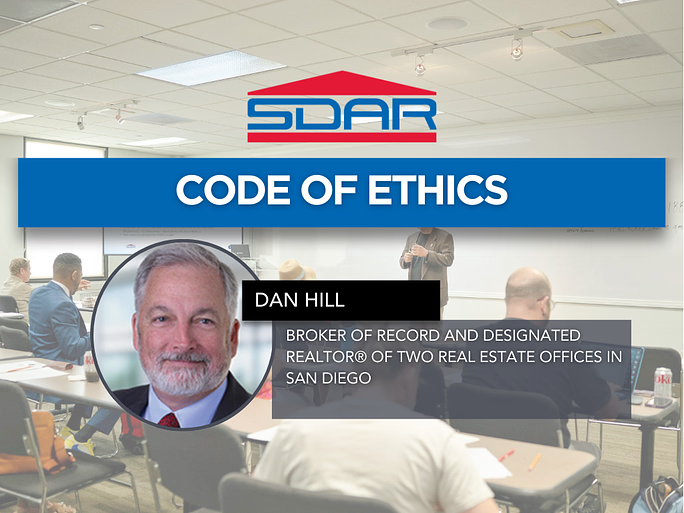

Strengthen your professionalism and protect your business by mastering the ethical standards that guide the real estate industry. This in-person course provides a clear and engaging overview of the National Association of REALTORS® Code of Ethics, the Standards of Practice, and the California Business and Professions Code that governs ethical conduct statewide.

Through real-world scenarios and practical analysis, you’ll learn how to navigate common ethical challenges, improve your client and peer relationships, and elevate the level of service you provide. Led by Dan Hill— industry leader and two-time Broker of the Year—this course delivers the insight and clarity only a seasoned mentor can provide. Dan’s expertise in supervision, risk management, and agent development brings depth and relevance to every discussion.

Participants will earn 3.00 hours of Continuing Education credit upon passing the required 15-question exam. Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 1 day before the session. Late registrants will not be admitted.

Classes

Buyer Consultation

A strong buyer consultation sets the tone for the entire transaction—and can be the difference between a smooth closing and a challenging relationship. Buyer Consultation is a practical, skill-building class designed to help REALTORS® deliver confident, professional consultations that convert prospects into committed clients.

Led by experienced REALTOR® and SDAR instructor Karen Van Ness, this course walks agents through how to structure an effective buyer consultation, clearly explain the buying process, establish expectations, and build trust from the very first meeting. You’ll learn how to communicate your value, address common buyer questions and concerns, and guide clients through timelines, financing, disclosures, and agency relationships with clarity and confidence.

Whether you’re working with first-time buyers or seasoned purchasers, this class provides actionable strategies and real-world insights to help you create stronger relationships, avoid misunderstandings, and position yourself as a trusted advisor throughout the home-buying journey.

Classes

Turn your open houses into a powerful, repeatable business-building system. Open Houses That Get RESULTS goes far beyond simply hosting an event. This class shows REALTORS® how to proactively use open houses to generate listings, referrals, and future buyers. Led by renowned real estate coach and industry veteran Mike Marmion, the course breaks down exactly what to do before, during, and after an open house to maximize real results.

You’ll learn proven preparation strategies, neighborhood outreach techniques, conversation scripts, and follow-up systems that transform open houses from passive time-fillers into high-impact opportunities. With Mike’s straightforward, relationship-driven approach, agents will leave with a clear checklist and confidence to run open houses that consistently create momentum, visibility, and income.

Classes

Listing Presentation

Winning the listing starts with a confident, well-structured presentation. Listing Presentation is a practical, results-driven class designed to help REALTORS® stand out in competitive listing appointments and consistently secure seller clients.

Led by experienced REALTOR® and SDAR instructor Karen Van Ness, this course breaks down how to deliver a polished, professional listing presentation that clearly communicates your value. You’ll learn how to guide sellers through the listing process, explain pricing and market data, outline marketing strategies, and address common objections with confidence. The class also focuses on setting expectations, building trust, and positioning yourself as a knowledgeable advisor who puts the client’s goals first.

Whether you’re new to listing appointments or looking to refine your approach, this session provides actionable strategies, real-world examples, and practical insights to help you present with clarity, credibility, and consistency—and walk away with more signed listings.

Classes

Building Your Sphere

Your sphere of influence is the foundation of a sustainable, referral-driven real estate business. Building Your Sphere is a practical, mindset-shifting class designed to help REALTORS® intentionally grow, organize, and leverage their database to generate consistent business and long-term success.

Led by veteran real estate coach and industry leader Mike Marmion, this course focuses on working by referral rather than chasing transactions. You’ll learn how to identify the right people for your database, clean and strengthen your contact list, and build meaningful relationships that position you as a trusted advisor. The class also covers simple daily habits, conversation strategies, and follow-up systems that turn your sphere into “walking, talking billboards” for your business.

Whether you’re new to real estate or looking to refocus your efforts, this session provides a clear, actionable framework for building a high-quality sphere that supports predictable growth and a lasting professional reputation.

Classes

Everything VA

Ready to confidently serve veterans, active-duty service members, and their families while expanding your business? Everything VA is a practical, agent-focused class designed to help REALTORS® understand the realities of VA loans and use them effectively in today’s competitive market. Led by top VA loan expert Clay Murray, this course breaks down VA eligibility, entitlement, property guidelines, and offer strategies—while separating common myths from facts.

You’ll learn how VA loans really work, how to position VA buyers competitively, navigate lender overlays, handle inspections and appraisals, and avoid common pitfalls that can derail transactions. Whether you’re new to VA deals or want to sharpen your expertise, this class will equip you with the knowledge, tips, and confidence to close more VA transactions while providing exceptional service to those who have served.

Classes

New Member Orientation

Start your real estate career with confidence at SDAR’s New Member Orientation. Designed for newly licensed REALTORS®, this essential session will walk you through everything you need to know to launch your business, understand your professional responsibilities, and make the most of your SDAR membership.

You’ll learn how to access and use your core member benefits, explore the tools and services included with your SDMLS subscription, and gain a foundational understanding of REALTOR® ethics, professional standards, and compliance requirements. The program also includes an overview of SDAR’s support teams, legal resources, market tools, industry advocacy, and opportunities for networking, education, and community involvement.

Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 1 day before the session.

Classes

Code of Ethics

Strengthen your professionalism and protect your business by mastering the ethical standards that guide the real estate industry. This in-person course provides a clear and engaging overview of the National Association of REALTORS® Code of Ethics, the Standards of Practice, and the California Business and Professions Code that governs ethical conduct statewide.

Through real-world scenarios and practical analysis, you’ll learn how to navigate common ethical challenges, improve your client and peer relationships, and elevate the level of service you provide. Led by Dan Hill— industry leader and two-time Broker of the Year—this course delivers the insight and clarity only a seasoned mentor can provide. Dan’s expertise in supervision, risk management, and agent development brings depth and relevance to every discussion.

Participants will earn 3.00 hours of Continuing Education credit upon passing the required 15-question exam. Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 1 day before the session. Late registrants will not be admitted.

Events

2026 New Laws & Industry Outlook

Join Us for the 2026 New Laws and Industry Outlook!

The Greater San Diego Association of REALTORS® invites you to the annual New Laws and Industry Outlook on Wednesday, February 4, 2026 at the The Legacy Resort Hotel & Spa in Mission Valley. This premier event will feature insightful presentations from key leaders shaping the real estate industry.

The Legacy Resort Hotel & Spa (Event center)

875 Hotel Circle South San Diego CA 92108

Registration & Breakfast 7:30 AM - 8:30 AM

Program from 8:30 AM - 3:00 PM

Highlights:

Economic Update, Josh Romney

2026 New Laws, Gov Hutchinson

Events

Global Real Estate Spotlight: Dubai & UAE Opportunities

Join us for a 15-minute exclusive presentation highlighting real estate investment opportunities in the UAE, with a special focus on Dubai and the landmark Mercedes‑Benz x Binghatti master-planned community.

This fast-paced briefing is ideal for REALTORS® interested in global markets, luxury developments, and cross-border investment opportunities.

Perfect for members exploring international real estate, investor clients, and Dubai-focused opportunities.

Classes

Counseling & Advising Buyers

Counseling & Advising Buyers is an essential course for REALTORS® who want to confidently guide buyers through the legal, contractual, and practical complexities of a real estate transaction. Led by attorney, broker, and risk management expert Jacqueline A. Oliver, Esq., this class focuses on helping agents explain contracts clearly, manage buyer expectations, and reduce liability at every stage of escrow.

Participants will learn how to simplify and communicate key contract provisions, navigate investigations and disclosures, handle deposits and contingencies, and properly use Notices to Perform and Demands to Close Escrow. This class provides practical guidance and legal insight to help REALTORS® protect their clients, minimize risk, and deliver informed, professional buyer representation from contract to close.

Classes

California’s Housing Market: Navigating Rates, Demand & Change-Webinar

Staying ahead of the market starts with understanding what’s next. Join this free virtual panel hosted by the Center for California Real Estate (CCRE) for expert insights into where California’s housing market is headed — and what it means for your business.

What you’ll gain:

A clear look at interest rates, buyer demand, and market shifts

Data-driven insights to help guide client conversations

Expert economic perspective moderated by Jerry Nickelsburg, UCLA Anderson Forecast

Wednesday, February 11

⏰ 10:00–11:15 AM

💻 Free for C.A.R. members | Virtual

Classes

Unraveling The Mystery of 1031 Exchanges

Unraveling the Mystery of 1031 Exchanges is a practical, Realtor-focused class designed to demystify one of the most powerful wealth-building tools available to real estate investors. Led by Bill Exeter, CEO of The Exeter Group and a nationally recognized authority with more than 45 years in financial services, this course breaks down 1031 exchanges in clear, real-world terms agents can confidently apply in transactions.

From a REALTOR®’s perspective, the class covers what truly qualifies as like-kind property, required holding and reinvestment thresholds, and the critical 45-day identification & 180-day completion deadlines. Agents will also gain insight into qualified trust and escrow accounts, forward and reverse exchanges, improvement exchanges, and foreign property exchanges - along with common misconceptions that can put deals and clients at risk.

This session equips REALTORS® with the knowledge needed to spot 1031 opportunities, communicate effectively with investors and advisors, and add measurable value to investor clients while staying compliant with IRS requirements.

Classes

Riches in the Niches: Winning Business in Today’s Market

Riches in the Niches: Winning Business in Today’s Market is a high-impact, strategy-driven class designed to help REALTORS® stand out, specialize, and thrive regardless of shifting market conditions. Led by veteran real estate leader and master trainer Mike Marmion, this session explores more than 26 proven niche strategies that help agents simplify their efforts, focus their energy, and dramatically increase profitability.

Participants will learn how to identify both focused niches (activity-based, predictable, and efficient) and lifestyle niches (authentic, relationship-driven, and aligned with personal interests), and how to strategically combine both for consistent results. The course breaks down how to choose the right niche, understand the numbers behind it, create a clear daily and weekly action plan, and position yourself as a “specialist” in the eyes of the public. Ideal for agents looking to gain clarity, differentiation, and long-term momentum through smart specialization.

Classes

Hard Money 101

Hard Money 101 gives real estate professionals a clear, practical understanding of hard money lending—what it is, when to use it, and how it can help clients close transactions that traditional financing can’t support. Taught by lending veteran Ted Przybylek, i.e. Rancho Ted’, a 30+ year industry expert known for solving complex buyer and seller scenarios, this course breaks down asset-based lending, true bridge loans, investor-funded financing, and real-life case studies that illustrate when hard money is the right tool.

Learn how to identify situations where speed, flexibility, or property conditions make hard money a smart solution, and gain the confidence to guide clients through alternative lending options that keep deals alive. This class is ideal for agents working with investors, flippers, distressed sellers, or buyers facing lending challenges.

Classes

Cold Calling: From Phones To Paydays

Cold Calling: From Phones to Paydays is a high-energy, practical class designed to help REALTORS® confidently connect with sellers other agents never reach. Led by top-producing Broker-Associate and office manager David Jefferson, this session breaks down modern cold calling for today’s market - what works, what doesn’t, and how to turn conversations into appointments and listings.

You’ll learn how to shift your mindset, prepare effectively, and use proven scripts for FSBOs, expired listings, and neighborhood outreach. The course covers call structure, objection handling, follow-up strategies, and simple tracking metrics that build a consistent pipeline. Whether you’re new to cold calling or looking to sharpen your skills, this class will give you the tools, confidence, and systems to turn phones into paydays and create predictable business growth.

Classes

Open Houses That Get RESULTS

Turn your open houses into a powerful, repeatable business-building system. Open Houses That Get RESULTS goes far beyond simply hosting an event. This class shows REALTORS® how to proactively use open houses to generate listings, referrals, and future buyers. Led by renowned real estate coach and industry veteran Mike Marmion, the course breaks down exactly what to do before, during, and after an open house to maximize real results.

You’ll learn proven preparation strategies, neighborhood outreach techniques, conversation scripts, and follow-up systems that transform open houses from passive time-fillers into high-impact opportunities. With Mike’s straightforward, relationship-driven approach, agents will leave with a clear checklist and confidence to run open houses that consistently create momentum, visibility, and income.

Classes

Counseling & Advising Sellers

Counseling & Advising Sellers is a must-attend class for REALTORS® who want to confidently guide sellers through the legal and contractual complexities of a real estate transaction while minimizing risk. Led by attorney, broker, and risk management expert Jacqueline A. Oliver, Esq., this course focuses on helping agents clearly explain contracts, disclosures, and seller obligations in a way clients can easily understand.

Participants will learn how to navigate required disclosures and exemptions, handle amended disclosures and pre-existing reports, and properly use Notices to Perform and Demands to Close Escrow. This class provides essential legal insight and real-world guidance to help REALTORS® protect their seller clients, reduce liability, and manage transactions professionally from listing to close.

Classes

Open House FENG SHUI Staging

Open House FENG SHUI Staging introduces REALTORS® to the art and science of Feng Shui as a powerful tool to enhance property appeal and attract high-value offers. Taught by renowned Feng Shui Master Alex Zi, an expert with over 30 years of experience and more than 9,000 students worldwide, this course reveals how strategic design, color, energy flow, and timing can influence buyer perception and success at open houses.

Using Feng Shui principles, learn how to stage every part of a home, balance the five elements, and resolve common layout challenges such as T-sections and stair placements. You’ll also discover how to apply Feng Shui to your marketing materials and client interactions to create harmony, confidence, and prosperity in your business.

Classes

Code of Ethics

Classes

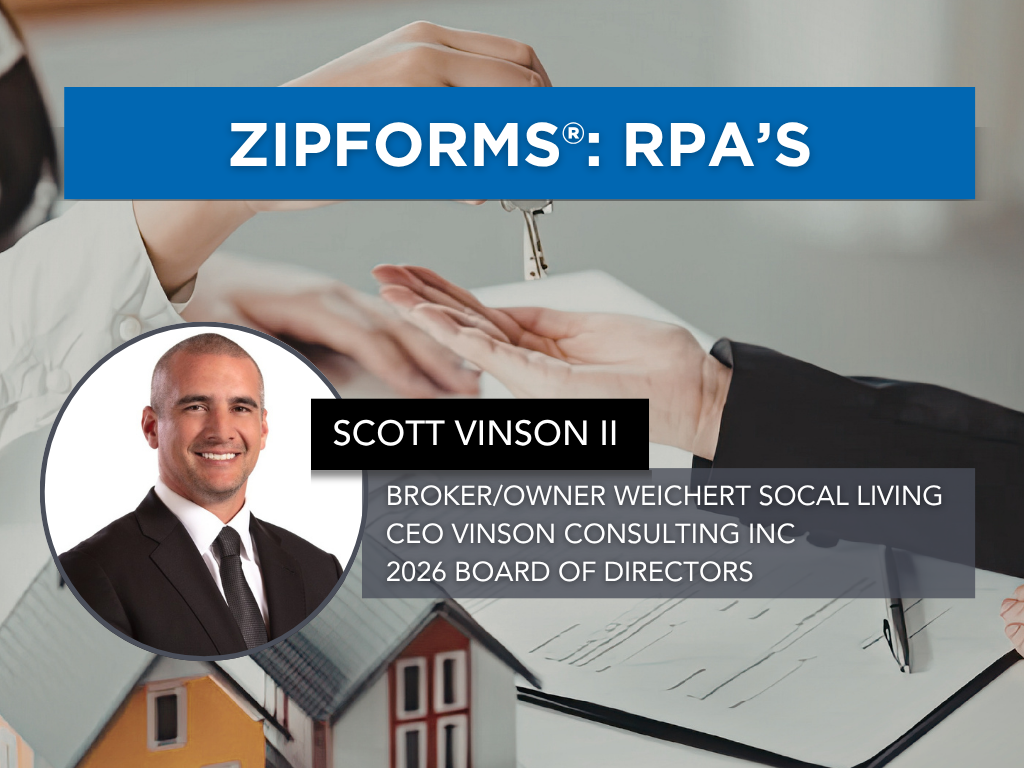

ZipForms: RPA's

Join us for an in-depth exploration of the ZipForms: RPA's, where esteemed REALTOR® and contract expert Karen Van Ness will guide you through the critical details of the Residential Purchase Agreement (RPA) form. Learn the nuances that will help you navigate your transactions with confidence and clarity. Whether you're new to the RPA or looking for a refresher, this class will enhance your proficiency in managing real estate contracts. Don't miss this opportunity to elevate your expertise and better serve your clients.

Events

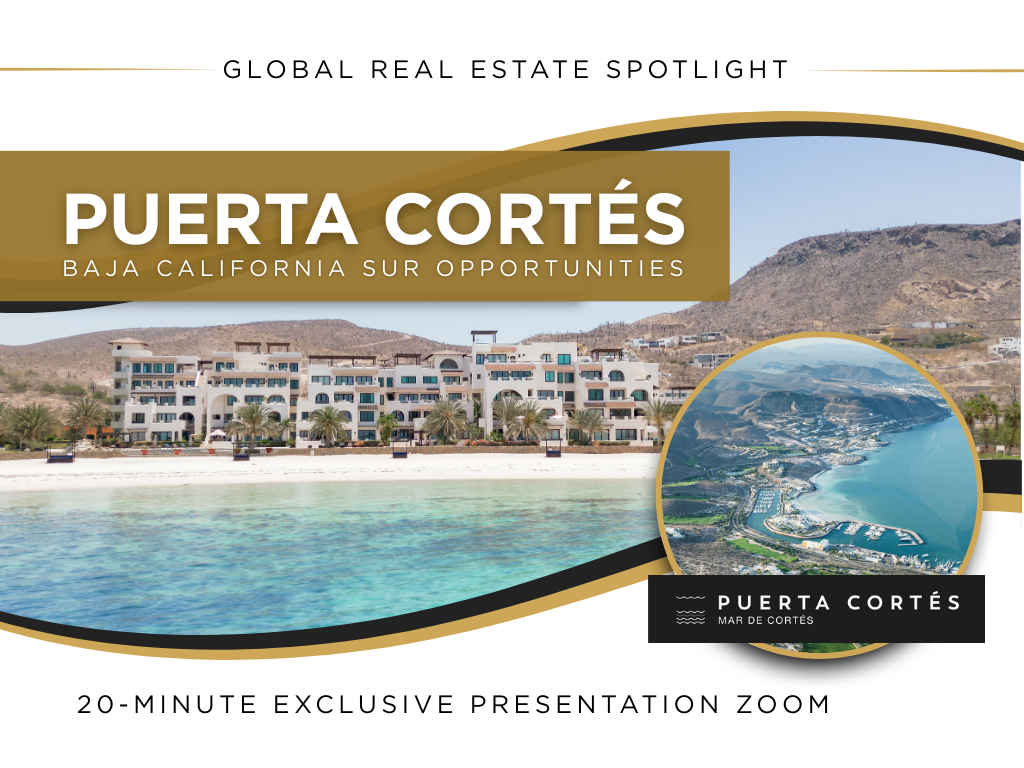

Global Real Estate Spotlight - Puerta Cortés, Baja California Sur

Join us for a 20-minute exclusive presentation during SDAR’s International Real Estate Committee meeting, featuring Puerta Cortés, one of Mexico’s premier master-planned coastal resort communities in La Paz, Baja California Sur.

This fast-paced market and opportunity update will highlight:

- Luxury residential and resort investment opportunities

- Marina, golf, and lifestyle-driven developments

- Cross-border buyer trends and U.S.–Mexico transaction insights

- Current inventory and future development phases

This presentation is open to all SDAR members.

Whether you work with investor clients, second-home buyers, or international referrals, this session will provide valuable global insight.

Zoom Link: https://us06web.zoom.us/meeting/register/3hMRNKobSeuOOyKWntLqJw

Classes

Unlocking Investment Transactions with 1031 Exchanges

Unlocking Investment Transactions with 1031 Exchanges reveals how real estate professionals can guide clients in leveraging the 1031 Exchange to build wealth, defer taxes, and achieve diverse investment goals. Led by Adam Nishikawa, a seasoned greater San Diego market expert with over a decade in real estate and eight years specializing in 1031 exchanges, this class covers top 10 strategic scenarios - from maximizing tax benefits and improving cash flow to facilitating out-of-state investing, estate planning, and portfolio restructuring.

Gain practical insights, compliance essentials, and communication strategies to work effectively with investors, agents, escrow officers, and CPAs - turning the 1031 Exchange into a powerful tool for your real estate clients’ long-term success.

Classes

Commercial Real Estate 101

This course provides real estate professionals with a foundational understanding of commercial real estate transactions and how they differ from residential deals. Participants will learn core commercial concepts, terminology, and transaction structures, gaining clarity on the unique dynamics of commercial properties.

Designed for residential agents interested in expanding into commercial real estate, this class delivers practical insights and real-world context to help participants identify opportunities, understand basic analysis, and recognize when and how to engage in commercial transactions. By the end of the course, attendees will have the confidence and knowledge needed to begin exploring commercial real estate opportunities and determine next steps in their professional growth.

Classes

ZipForms: RLA's

In the ZipForms: RLA's class, esteemed REALTOR® and contract expert Karen Van Ness will guide you through the current listing forms used in real estate transactions. Each form will receive dedicated attention, ensuring you gain a comprehensive understanding of how to effectively utilize these documents in your practice. Learn the nuances that will help you manage your listings with confidence and precision. Whether you're new to these forms or seeking a refresher, this class will enhance your proficiency in handling listing agreements.

Classes

Proactive Property Management Tips

Proactive Property Management Tips is a practical course designed to provide real estate professionals with proactive property management tips and strategies that maximize efficiency and minimize risk. This training covers essential topics including the importance of thorough tenant screening, crafting legally sound lease agreements, and implementing effective rent collection strategies. You will also gain insight into navigating lease renewals, handling evictions professionally, and attracting quality tenants through smart marketing.

Events

Circle of Excellence

The Circle of Excellence, hosted annually by the Greater San Diego Association of REALTORS®, honors outstanding REALTORS® and Brokers who demonstrate excellence in their profession, leadership in the industry, and a commitment to their clients and communities.

The Circle of Excellence recognizes achievement in both production and leadership. Whether your success is measured by performance, service, or impact, there is a category for you.

Select your award category and apply today.

https://www.sdar.com/circle-of-excellence/2025.html

Classes

Mastering Your Real Estate Schedule

Success in real estate isn’t about working more hours, it’s about working the right hours, on the right activities, consistently. Mastering Your Real Estate Schedule is a practical, strategy-driven class designed to help REALTORS® take control of their time, reduce stress, and build a schedule that drives real production.

Led by industry veteran Mike Marmion, this session breaks down how to design an intentional weekly and annual schedule that prioritizes dollar-producing activities, protects lead generation time, and creates balance without sacrificing growth. Agents will learn how to structure their days for focus and momentum, avoid common time traps, implement time-blocking strategies, and build systems that turn consistency into predictable results. If you’re ready to stop reacting to your calendar and start commanding it, this class will give you the structure, clarity, and confidence to get more done in less time while building a sustainable business.

Classes

Hard Money 101

Hard Money 101 gives real estate professionals a clear, practical understanding of hard money lending—what it is, when to use it, and how it can help clients close transactions that traditional financing can’t support. Taught by lending veteran Ted Przybylek, i.e. Rancho Ted, a 30+ year industry expert known for solving complex buyer and seller scenarios, this course breaks down asset-based lending, true bridge loans, investor-funded financing, and real-life case studies that illustrate when hard money is the right tool.

Learn how to identify situations where speed, flexibility, or property conditions make hard money a smart solution, and gain the confidence to guide clients through alternative lending options that keep deals alive. This class is ideal for agents working with investors, flippers, distressed sellers, or buyers facing lending challenges.

Classes

1031 Exchanges Unlocked

1031 Exchanges Unlocked is a practical, opportunity-focused class designed to help REALTORS® confidently introduce and navigate 1031 exchanges while creating more value and more business. Led by nationally recognized 1031 expert Aaron Kancevicius, this session breaks down the rules, timelines, and strategies behind tax-deferred exchanges in clear, real-world terms.

Agents will learn the fundamentals of qualifying a property, the critical 45-day and 180-day deadlines, identification rules, reinvestment requirements, and the role of the Qualified Intermediary. This class equips REALTORS® with the knowledge and confidence to spot opportunities, fulfill their duty of care, and help clients defer taxes, preserve equity, and build long-term wealth.

Classes

Your Sphere Marketing Blueprint

Your database is more than a contact list, it’s your most valuable business asset. Your Sphere Marketing Blueprint is a practical, step-by-step class designed to help REALTORS® turn everyday relationships into a consistent, referral-driven pipeline.

Led by industry veteran Mike Marmion, this session outlines a simple, repeatable annual marketing plan that any agent can implement, regardless of experience level or budget. You’ll learn how to organize and segment your database, create meaningful touchpoints throughout the year, stay top-of-mind without feeling salesy, and build authentic connections that naturally generate repeat and referral business. If you’re ready to stop guessing what to send and when, and start following a clear, strategic plan, this class will give you the structure, clarity, and confidence to make your sphere your strongest source of business.

Classes

Buyers of 2026 & The BRBC

Classes

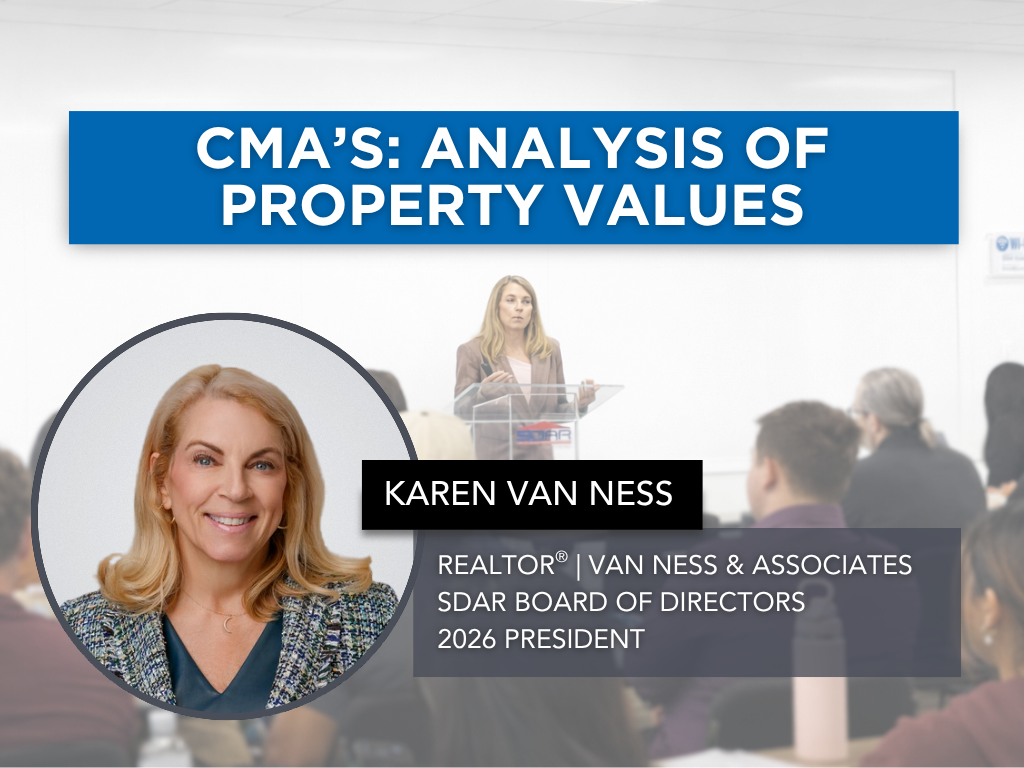

CMA's - Analysis of Property Values

Accurate pricing is one of the most critical skills in real estate and a well-prepared Comparative Market Analysis (CMA) is at the heart of every successful listing and buyer client consultation. CMA’s – Analysis of Property Values is a practical, hands-on class designed to help REALTORS® confidently evaluate property values and communicate pricing strategies with clarity and credibility.

Led by experienced SDAR instructor Karen Van Ness, this session explores the key components of a strong CMA, including selecting and adjusting comparable properties, analyzing current market trends, and interpreting economic related data to determine fair market value. Agents will also learn how to present their findings effectively to clients, support pricing recommendations, and position themselves as trusted advisors in competitive situations.

With a focus on real-world application and clear instruction, this class equips REALTORS® with the tools and insight needed to price properties accurately, guide client expectations, and make informed, data-driven decisions in today’s dynamic market.

Classes

New Member Orientation

Start your real estate career with confidence at SDAR’s New Member Orientation. Designed for newly licensed REALTORS®, this essential session will walk you through everything you need to know to launch your business, understand your professional responsibilities, and make the most of your SDAR membership.

You’ll learn how to access and use your core member benefits, explore the tools and services included with your SDMLS subscription, and gain a foundational understanding of REALTOR® ethics, professional standards, and compliance requirements. The program also includes an overview of SDAR’s support teams, legal resources, market tools, industry advocacy, and opportunities for networking, education, and community involvement.

Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 1 day before the session.

Classes

Code of Ethics

Strengthen your professionalism and protect your business by mastering the ethical standards that guide the real estate industry. This in-person course provides a clear and engaging overview of the National Association of REALTORS® Code of Ethics, the Standards of Practice, and the California Business and Professions Code that governs ethical conduct statewide.

Through real-world scenarios and practical analysis, you’ll learn how to navigate common ethical challenges, improve your client and peer relationships, and elevate the level of service you provide. Led by Dan Hill, industry leader and two-time Broker of the Year, this course delivers the insight and clarity only a seasoned mentor can provide. Dan’s expertise in supervision, risk management, and agent development brings depth and relevance to every discussion.

Participants will earn 3.00 hours of Continuing Education credit upon passing the required 15-question exam. Arrive early for check-in, have your SDAR Member ID ready, and bring a government-issued ID for verification.

Please note: Registration closes 1 day before the session. Late registrants will not be admitted.

Classes

2026 Q2 Business Boost and Recovery Plan

Consistent production in real estate starts with focused, income-generating activities, and having a clear plan to execute them daily. 2026 Q2 Business Boost and Recovery Plan is a practical, action-oriented class designed to help REALTORS® reset their routines, rebuild momentum, and drive results in a competitive and shifting market.

Led by experienced industry professional Mike Marmion, this session highlights the core activities that lead directly to business growth, including effective open house strategies, purposeful sphere outreach, proven conversation scripts, and relationship-building techniques. Agents will learn how to prioritize their time, increase meaningful client interactions, and implement simple, repeatable systems that generate leads and strengthen their pipeline.